")

")

")

")

The iShares Ethereum Trust ETF (ETHA) is an exchange-traded vehicle designed to give investors indirect exposure to Ether. This is the fund’s only holding (barring any cash held on its books), which results in a very high correlation to Ether (ETH-USD). The analysis outlined here isn’t an investment case for Ether. It’s a attempt to dispel some of the misconceptions around crypto investing. More importantly, I look at it as a way to learn more about the crypto currency, to understand the advantages and disadvantages of indirect ownership, and to use as a starting point to build your own investment case, either for or against. With that disclaimer out of the way, let’s move ahead.

The Ether and Ethereum Confusion

Crypto newbies might be under the impression that these two terms are synonymous and can be used interchangeably, and that’s made worse by the fact that the ETF refers to itself as an “Ethereum” trust. In fact, in common usage, people speak of Ethereum as the crypto, which isn’t accurate.

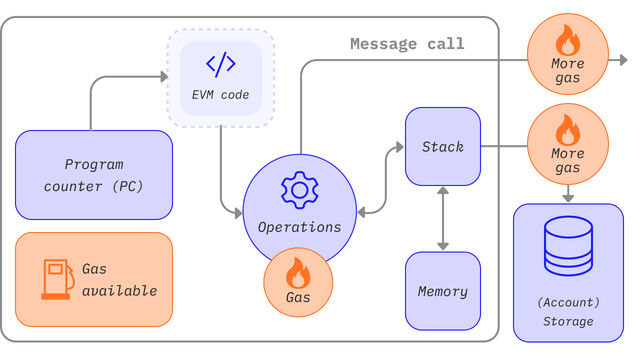

Technically speaking, these are two related but completely different things. Ethereum can be thought of as the decentralized blockchain infrastructure or network that smart contracts are executed on and decentralized applications or DApps are deployed and run on. Ether is the digital token or currency that pays miners and validators to process and authenticate these transactions.

The computation of these transactions is done on EVMs or Ethereum Virtual Machines, which in turn run on the blockchain’s nodes. When these nodes run the EVM environment, the computational effort is compensated for in the form of Ether, which is integral to running these operations because it acts as the fuel. That’s why these crypto payments are also called “gas fees”.

Ethereum.org

It should be clear by now that you can’t trade Ethereum (though “trading Ethereum” is commonly accepted in parlance), but since it’s so widely used to refer to the crypto rather than the blockchain network, it can be confusing. Ether, on the other hand, can be traded, which is where ETHA comes into the picture.

The “Trust” Confusion

We’re not done yet! You may have noticed that a lot of ETFs have “trust” in their names, just like ETHA does, and this is even more of a head-scratcher.

A true Trust ETF is also called an Investment Trust, which is also different from what’s known as a Unit Trust, which isn’t listed. An Investment Trust is listed, but it’s closed-ended, which means the share count is fixed, and the value comes from the shares trading at either a discount or premium to the net asset value or NAV. They don’t have the creation/redemption process that would make them open-ended.

Trust ETFs like ETHA and even the almighty Invesco QQQ Trust (QQQ) are different because they’re open-ended, but even these are dissimilar because one is a commodity trust holding ETH-USD, while the other is an equity trust holding equities or company stocks.

In the context of ETHA, the word “trust” refers to the legal structure of the fund. It’s like a trust that holds a tradable instrument called Ether. It’s not an Investment Trust or a Unit Trust.

If you’re still confused, let me try putting it a different way. The confusion mainly arises from the multifaceted usage of the term “trust”. In the UK, an Investment Trust or a Trust ETF is what investors in the U.S. would call a CEF or closed-ended fund. Now, what U.S. investors would call a Trust ETF is a Grantor Trust, or a legal wrapper that holds a single commodity, which in the case of ETHA is Ether. QQQ is different in that U.S. investors would call it a UIT or Unit Investment Trust. It’s actually among the first ETF legal structures to be introduced to the market.

The best way to wade through this mess of legalese is to stick with the American usage, so ETHA is basically a grantor trust that holds Ether as its commodity. We’ll stop before we get into the weeds with this, if we’re not there already!

Note: I haven’t provided any source links for the above because these are well-known facts within the professional investment community. Retail investors don’t really need to know these things in order to trade ETHA, so please treat this as more of academic or educational exercise, which is what this article is meant to be. Having said that, there are a few things that are important for investors to know, and that’s what I’ll dive into next.

ETHA and the Advantages and Disadvantages of Indirect Crypto Ownership

ETHA is a Delaware Statutory Trust, that’s what matters. At its core, this status gives investors, chiefly institutional, the necessary regulatory and legal compliance protection to be able to invest in digital tokens. The fund itself holds physical crypto assets through a custodian, which in this case is Coinbase Prime, owned by Coinbase Global, Inc. (COIN) the namesake exchange’s trading platform.

As a retail investor, when you buy ETHA, what you’re actually doing is buying a share of these Ether holdings, but because there’s no direct, physical or digital ownership, you can’t use the Ether to transact on a blockchain the way you would if you held ETH-USD directly, in a crypto wallet.

You have to know this because an ETHA holding doesn’t allow you to use DApps, it doesn’t give you the privacy that direct ownership does, and you don’t technically have full control over your holdings other than the ability to buy or sell the ETF shares.

On the flip side, the advantage of an indirect holding is that you don’t have to worry about keeping your seed phrase secure, you don’t need to trudge up the steep technical learning curve involved in setting up a crypto wallet and ensuring its security, and not being able to transact means not accidentally sending money to the wrong person, which is irreversible in a decentralized environment.

Investing in ETHA

We’re covered a lot of background so far, so now it’s time to get into ETHA and what being invested in this ETF involves.

Since this is an educational article, I won’t be making a recommendation either way, but let’s look at some ETF basics and try to understand what moves the price of Ether — or Ethereum, colloquially speaking.

ETHA was incepted on June 24, 2024, and holds Ether as its sole portfolio security. As of April 9 its market value is $6.76 billion. This is the bulk of its $6.86 billion in net assets under management or AUM.

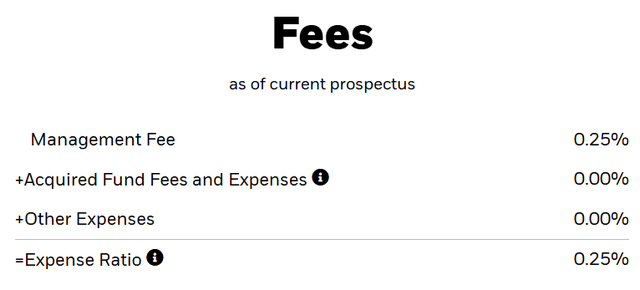

As this is a passively managed fund, its ER or expense ratio, also called a “sponsor fee”, is 0.25%. You’ll find SA reports a figure of 0.12%, but I’m not sure where that data’s from. From the ETHA website:

ETHA Fact Sheet

The shares are created and redeemed in batches of 40,000 known as “baskets” by what are known as authorized participants or APs, and are traded on the NASDAQ. Since this is a passive fund, the Trust doesn’t use any kind of derivatives leverage, nor does it trade ether to buy low and sell high. What you see is what you get. It tracks the price of ether, nothing more, nothing less.

What Are The Risks Involved in an ETHA Investment?

The ETF tracks the price of ether, which means it is highly dependent on the value assigned to this cryptocurrency and its acceptance within the broader context of digital currencies. That’s the biggest risk here.

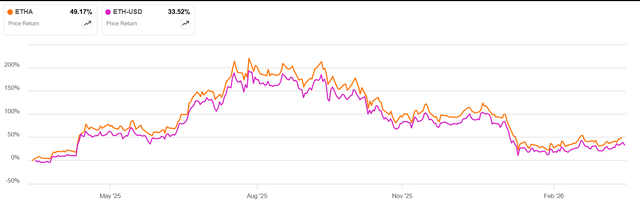

There’s also volatility risk because cryptos by nature undergo significant fluctuations in value driven by the underlying demand-supply dynamic, so don’t be surprised by the 73% volatility this ETF experiences on an annualized basis. That’s usually a given when investing in any cryptocurrency. Not surprisingly, that 73% is on the low side for a crypto because ether is among the more dominant cryptos, second only to Bitcoin (BTC-USD).

You won’t see a turnover risk because there’s no rebalancing, only the basket creation and redemption processes that affect the ETF’s AUM. More demand means more baskets of 40,000 shares each being created, and the converse holds true.

The Right Way to Understand the Performance of ETHA against ETH-USD

SA

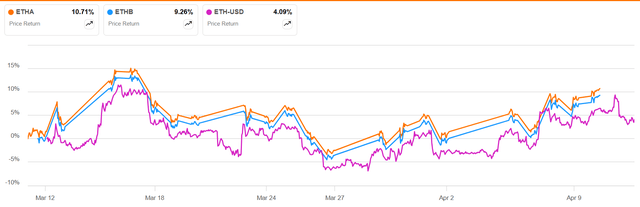

As if we didn’t have enough to be confused about, there’s another nuance with ETHA and its newer cousin, the iShares Staked Ethereum Trust ETF (ETHB), which was launched about two months ago.

Let’s get that one out of the way first. ETHB uses a different strategy and intends to pay distributions, unlike ETHA. The strategy to generate income is called “staking”, and you can learn more about that here. The simple way to explain this is to compare it to lending your stocks to other investors to borrow towards short positions they hold. There are major differences, though, so it’s not exactly an apples to apples comparison, but it serves the purpose of this discussion. What’s similar is that both strategies (staking and lending) result in generating a passive income stream. That’s why ETHB is able to commit to a distribution, although that hasn’t yet started.

But ETHA doesn’t engage in staking, so why does it look like it’s outperforming ETH-USD, which should theoretically be impossible?

SA

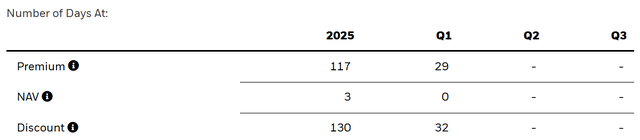

The first factor pushing ETHA up is strong institutional demand ahead of the “Glamsterdam Hard Fork” slated for H1 2026. I’m not getting into the technical aspects here, but it’s aimed at increasing the efficiency and throughput of the Ethereum blockchain. That demand creation means ETHA is currently trading at a premium to its NAV, the NAV being the actual price of the ether it holds. The premium is currently at 0.33% as of April 10. It’s a little down from 0.60% earlier in the year, and that could be because of potential delays announced a few days ago. Of course, over time, this will evolve.

So this premium to NAV dynamic makes it look like ETHA is outperforming ETH-USD in terms of price.

Another dynamic for investors to be aware of comes from the trading hours of ether as opposed to the trading hours of NASDAQ. Since the former trades 24/7, if ether sees a rally during NASDAQ off hours, such as the weekend for example, Monday morning 9:30am Eastern, you’ll see ETHA gap up. On the other side of the coin, if ether drops over the weekend but recovers before the stock market opens, ETHA’s price chart will look like nothing happened. It’s the gaps-up/down that account for this optical illusion, but it’s mainly the premium to NAV that’s responsible for any outperformance that you see.

The second factor underlying this outperformance is triggered when short positions are high. When ether begins to recover after a drop, short-sellers rush to cover their positions, Since institutional investors generally use the ETF rather than the crypto itself to hedge these short positions, ETHA benefits from this squeeze.

These multiple dynamics may make it look like ETHA is a better holding than a direct ether investment, but it’s also true that the ETF’s market price has traded at a discount to NAV more often than at a premium.

ETHA website

I hope this article has been a bit of a revelation for investors who are unfamiliar with the crypto landscape and investing in ether, and I’d really appreciate it if seasoned crypto investors could share their expertise with others in the comments.

This article answers three main questions about ETHA:

- How is ETHA structured?

- What impacts ETHA’s price movement?

- How can ETHA fit into a portfolio?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Read the full article here

")

")

")

Shareholder/Analyst Call Transcript")

")

")

")

")

")